We will be layering original analysis into our FP&A in the Trenches newsletter to keep modern finance leaders up-to-date with current trends and how they impact planning and analysis.

This continues from last week’s article: Mastering the Predictable Surprise: Let’s get to work.

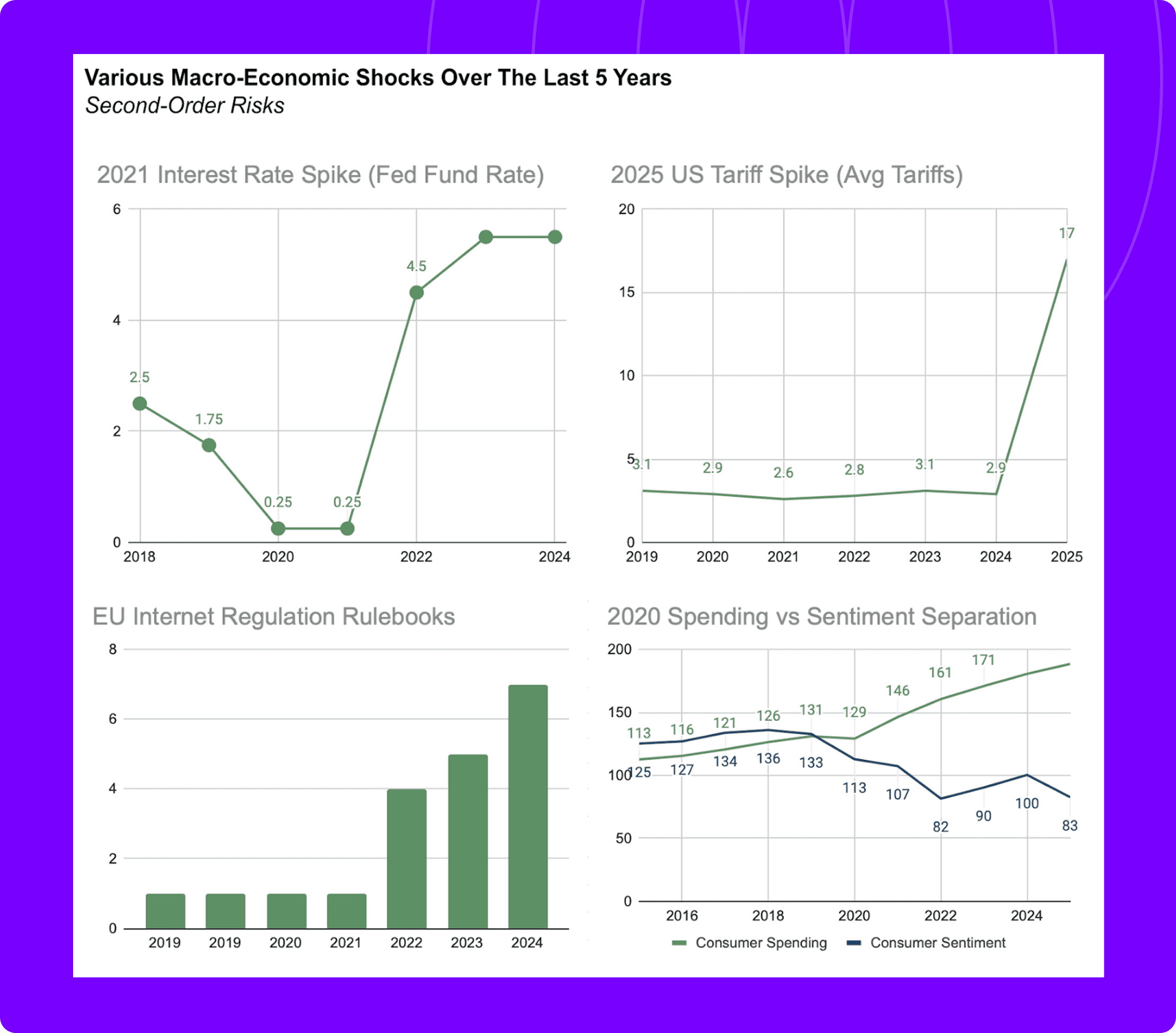

Source: St. Louis FRED, Yale Budget Lab, Publications of EU, St. Louis FRED

The Bullets

|

Here are two quick stories that show how uncertainty actually hits you. First, driving. Most of us think we are good drivers. But, accidents are rarely caused only by the one or two drivers involved. Many times it is a chain reaction. One car swerves to avoid another, a third car brakes late, and a fourth car has nowhere to go. The difficulty is the chaotic interaction. Company ecosystems behave the same way.

The second, more topical story. A company I was invested in started to grow quickly. The product was good. The pipeline was real. Then, government funding priorities changed. Overnight, many of their customers across several industries paused payments, including on contracts they already owed. The company had never taken government money. Their users did, and those users stopped paying. Collections slowed, runway shortened, and the business eventually closed. It was not a product failure. It was a second-order risk that turned into a liquidity crisis.

Here is the lesson for finance leaders. You are not managing a set of isolated drivers. You are managing interactions. Your plan needs to hold up when someone else swerves to dodge their own risk. So, it's worth identifying the major risk to your customers, suppliers, and funders, whether that be a commodity move, regulatory change. If you can see these dependencies clearly, you can create room to maneuver quickly during a crisis.

Domain | Traditional FP&A View (First-Order Thinking) | 10x CFO Thinking (Second-Order Thinking) |

|---|---|---|

Core Question | "Are we doing okay?" | "Is our ecosystem (customers, suppliers, partners) okay?" How can we help? |

Scenario Planning | Simulate internal shocks (e.g., lost revenue, cost spikes) | Model ecosystem shocks (e.g., customer default → supplier delay → margin compression) |

Risk Focus | "What is our cash burn?" | “What is our customer's cash burn?" |

CapEx | Prioritize internal ROI | Funding partners that accelerate our market |

Here's how to identify the impacts, some notes on mitigations, and finally how to track them on an ongoing basis.

What drives the revenue of your customers?

As the saying goes, you need to understand your customers. Not only what they are using you for, but how your services are providing their customers value. For at least the top half of your portfolio, you need to understand:

Who are your customers relying on to make money?

What are the major drivers that impact their revenue?

How significant are you to their revenue?

As an added bonus, this is just great information for your team to have to identify the future direction that your company grows to add value.

Some ways to mitigate: Diversify your customer base, use flexible payments during hardship, usage floors to reduce volatility of demand swings, prepayment and milestone billing.

What drives the revenue of your suppliers?

I was listening to an equity analyst speak. He proudly noted how he hadn’t slept for days because of an earthquake. He was covering a company that wasn’t directly impacted, but had a spreadsheet on all of the major suppliers of the company and where those subcontractors had factories. It turned out one of the sub-sub-suppliers had an impacted factory that would materially slow down the revenue of the company he covered.

If an outside analyst was able to figure it out, you should know it.

Who are your supplier’s top customers?

How robust is their supply chain? Where is it geographically?

Who has more leverage in the relationship?

What are your backup options?

As McKinsey recommends, more and more CFOs should take an active role in the procurement chain because of its bottom-line effects. By jumping on this early, you will be able to mitigate the knock-on effects.

Some ways to mitigate: Diversify sourcing geographically, strengthen supplier relationships, maintain an inventory buffer, place large orders before the worst hits.

What about your funders?

In 2022, interest rates increased, leading to higher pressure on funders to deliver strong returns. Among various reasons, this slowed the flow of capital that many startups were expecting to tap. Companies that saw early signs of this were able to raise a lot of money before interest rates kept rising and venture capital deals slowed down.

On a different note, the explosion of private credit has supplemented bank lending. Companies that tapped into this network quickly have been able to tap a huge pool of additional credit. Though, of course, now with the failings of First Brands and Tricolor private credit is under the microscope.

The point is, it behooves you to know what will impact your sources of capital. The checklist here remains the same, so I won’t bullet it out. But who do your funders depend on, and how important are you to their portfolio?

Some ways to mitigate: Set up a credit line, cycle debt repayment windows, hold at least two years of cash needs for growth.

Finding your canaries in a coal mine

Of course, once you start going down this rabbit hole, it’s never-ending. What about their suppliers and their suppliers’ suppliers and their raw materials and the economic outlook of each country across the world? Suddenly your spreadsheet will have so many variables and so much confusion that it will be rendered useless for moving quickly.

Instead, you should focus on a few high-level metrics that impact your counterparties, that you can get publicly. To do this:

Batch your key relationships. Across suppliers, funders, and customers what are the key variables that have an outsize impact on their business?

Identify the common macroeconomic variables. List out the key variables and make a back-of-the-envelope analysis of potential effects across the ecosystem.

Keep an eye on any relevant regulatory issues. Know what relevant regulations for major businesses are being discussed by setting up news alerts.

Model out the impact. You need to assess how much these microeconomics will hurt your counterparties and how much that will impact you.

(un)Surprisingly, very few others at the company will be thinking through these things, so offer to take it over as part of the finance role and offer the occasional update in monthly meetings.

Tip: This isn’t a one-time analysis. So make sure you assign a team member to own this ongoingly.

In conclusion

Second-order impacts are notoriously difficult to predict. But you don’t need to. What you need to do is know your ecosystem and monitor the key drivers. This will ensure that when the cars three ahead stop, you can slow down to avoid a crash.