Since 2022, we’ve entered the age of the operator. Multiples are tighter than they were a few years ago. Deal activity has not slowed. IRRs have not magically improved. That gap has to be made up somewhere. And it is being made up through execution.

This is why the first 100 days matter more now than at any point in the last decade. Value creation is no longer something you “get to” once the dust settles. It has to start immediately.

Every deal begins with a thoughtful, detailed 100-day plan. And yet, if you spend time inside enough portfolio companies, you start to see the same pattern.

Around Day 60, the plan starts to drift. Not because the ideas and strategy were wrong. Because the finance system inside the company was never built to operationalize them.

Initiatives live in slide decks. Savings do not show up clearly in the General Ledger. Revenue grows while margin quietly erodes. EBITDA improves while cash gets tighter. Board packs tell a story of progress, while IRR slowly slips beneath the surface.

Here are the seven places 100-day plans tend to break, and what to put in place early to stay on track.

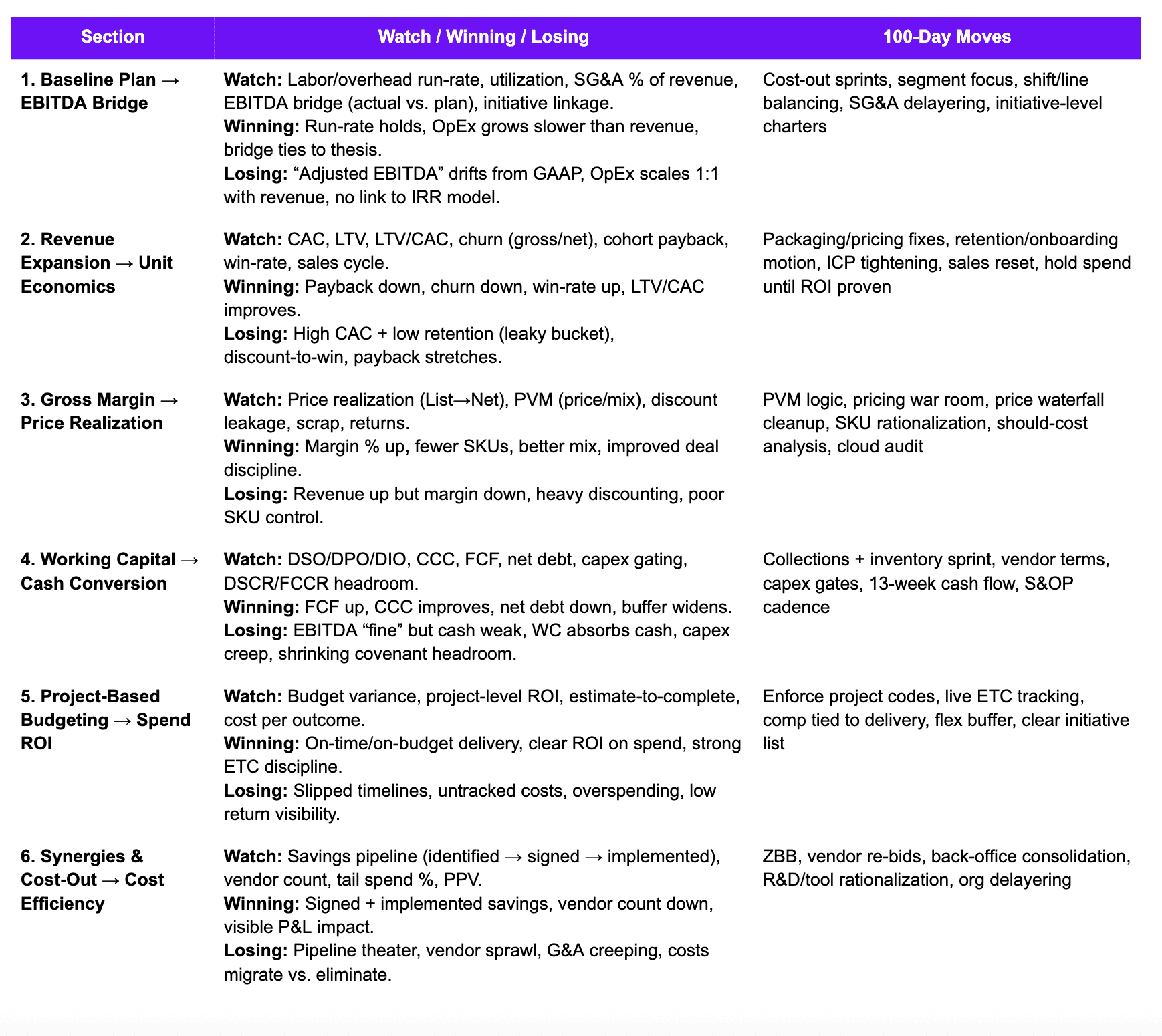

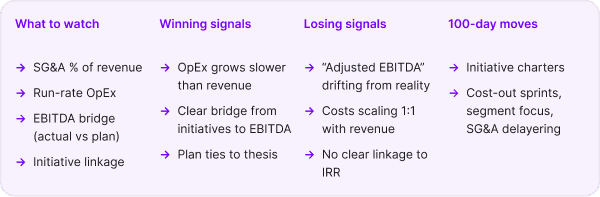

1. Make the Baseline Plan

What the playbook says

Start with a clean bridge from ARR and churn to the LBO model. Map every initiative directly to a financial outcome so the operating plan and the investment thesis are perfectly aligned from Day 1.

What actually happens

The bridge is included in the model and the kickoff deck. Then the deal closes and real systems take over.

By the second month, ask how initiative savings show up in EBITDA, and you will get vague answers. The investment thesis lives in one world. The General Ledger lives in another. Adjusted EBITDA starts to tell a story that feels directionally right but is increasingly detached from how the business actually runs.

Thoma Bravo's acquisition of Ellie Mae worked because this did not happen. Pricing changes and TAM expansion were not just strategic moves. They were moves that could be traced, line by line, back to the financial model. That is why the growth translated into real value creation, not just revenue growth.

What to do differently

The first priority is not new analysis. It is plumbing - one version of the truth across ERP, CRM, and HRIS.

A clear definition of how benefits are calculated before initiatives even begin.

Initiative charters that reconcile directly to the capital model.

Sequence work based on what the organization can actually absorb, not what the plan says should happen.

Tip: Your 13 week cash flow will be your constant companion to ensure you have control of the business.

2. Revenue Expansion

What the playbook says

Cross-sell customers. Expand the product surface area. Open new channels. Show growth early in the hold period to build momentum.

What actually happens

Revenue responds, which is reassuring. The dashboards start trending in the right direction. Sales feels energized. The board sees progress.

Underneath, CAC starts creeping up. Discounting becomes more common than anyone wants to admit. Retention issues stay buried inside cohorts that are not examined closely enough. The company is spending heavily to acquire revenue that looks good in the top line but does very little to improve the exit multiple. By the time finance sees this clearly, the motion is already in full swing and expensive to unwind.

Marketo is a useful contrast. The early focus after acquisition was not on adding more product or opening more channels. It was on fixing the sales engine and cost structure so that growth would be profitable when it came. ARR doubled because the economics were addressed first, not after.

What to do differently

Slow the motion down before accelerating it.

Map whitespace at the account level before launching expansion plays.

Study churned and non-repeat customers to understand where onboarding, support, or pricing is breaking down.

Watch CAC, payback, LTV, and discount behavior weekly, not quarterly.

Put real gates on GTM spend so economics lead growth instead of following it.

Tip: If your CAC payback period exceeds 18 months, you’re likely burning cash for revenue that won’t move your multiple at exit.

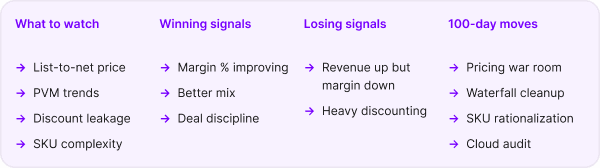

3. Gross Margin

What the playbook says

Run price-volume-mix analysis. Review pricing. Audit cloud and infrastructure costs. Improve gross margin.

What actually happens

Deals need to close. Discounting becomes the fastest lever to hit targets. Legacy pricing structures hide true contribution margins. Engineering time gets consumed supporting customers who never truly pay back what they cost to serve.

Revenue trends up. Margin trends down. And it is surprisingly hard to see in standard reporting because the systems were never built to isolate where price, mix, and volume are helping or hurting.

Dynatrace is instructive here. Forcing a cloud-only pivot was not just a product decision. It removed a pricing and operational model that had been masking margin and consuming resources for years.

What finance must do differently

Treat PVM as an operating discipline, not an analytical exercise.

Build a real price waterfall that exposes list-to-net leakage.

Look at cloud and infrastructure costs as margin work, not IT hygiene.

And be willing to migrate or part ways with customers whose support burden outweighs their contribution.

Tip: Tie GTM spend gates to LTV/CAC and payback period thresholds. Any % improvements will help across all multiples at exit.

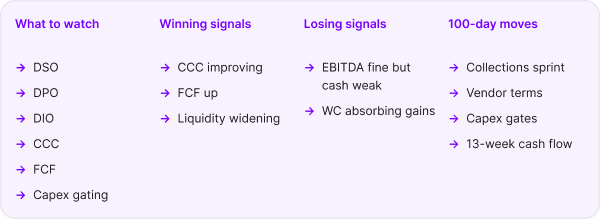

4. Working Capital

What the playbook says

Run price-volume-mix analysis. Review pricing. Audit cloud and infrastructure costs. Improve gross margin.

What actually happens

Deals need to close. Discounting becomes the fastest lever to hit targets. Legacy pricing structures hide true contribution margins. Engineering time gets consumed supporting customers who never truly pay back what they cost to serve.

Revenue trends up. Margin trends down. And it is surprisingly hard to see in standard reporting because the systems were never built to isolate where price, mix, and volume are helping or hurting.

Dynatrace is instructive here. Forcing a cloud-only pivot was not just a product decision. It removed a pricing and operational model that had been masking margin and consuming resources for years.

What finance must do differently

Treat PVM as an operating discipline, not an analytical exercise.

Build a real price waterfall that exposes list-to-net leakage.

Look at cloud and infrastructure costs as margin work, not IT hygiene.

And be willing to migrate or part ways with customers whose support burden outweighs their contribution.

Tip: Fix packaging and pricing to loosen up inventory and speed up shipping times where applicable.

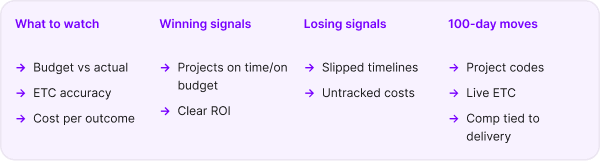

5. Project-Based Budgeting

What the playbook says

Tie spend to projects. Track ROI. Allocate capital in line with value creation priorities.

What actually happens

Budgets slowly drift back into departments. Project lists grow but lose prioritization. Costs are incurred without anyone being able to explain how they tie back to the original plan.

The organization stays busy. Work is happening everywhere. The connection to value creation quietly fades. By the second month, the initiative list in the kickoff deck looks very different from how money is actually being spent.

What finance must do differently

Require project codes at the requisition stage so costs are tagged from the start.

Track the estimate-to-completion every week so overruns are visible early.

Keep a living, visible initiative list tied directly to the thesis.

Align compensation with project delivery rather than functional activity.

Tip: Consider including a flex fund buffer to the budget to keep up with the quick pace.

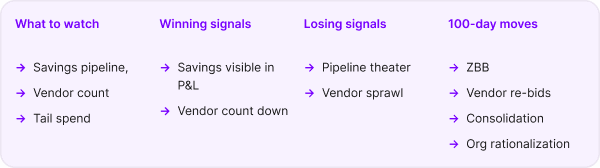

6. Synergies & Cost-Out: Less Headcount, More Output

What the playbook says

Consolidate functions. Reduce headcount. Run zero-based budgeting. Capture synergies.

What actually happens

Savings are identified in workshops and spreadsheets. Vendors remain. Costs shift from one department to another. The organization stays layered because structural change is uncomfortable and slow.

On paper, there is a healthy pipeline of savings. In the P&L, much less evidence. What was meant to be a one-time reset turns into a long, slow effort that loses urgency.

What to do differently

Move quickly to consolidate back-office functions.

Rebid vendors and aggressively eliminate tail spend.

Benchmark spans and layers to remove management bloat.

Force quarterly kill versus accelerate reviews so capital gets redeployed rather than diluted.

Tip: With AI ramping fast, expect back-office efficiency benchmarks to get even tighter. You’ll need systems that do more with less.

7. Control

What the playbook says

Improve close speed. Implement rolling forecasts. Deliver high-quality board packs.

What actually happens

Forecast error is rarely measured explicitly. Initiative drift hides inside aggregated numbers. Reporting starts to tell a reassuring story rather than highlighting what is off track.

The board feels informed. The operators feel busy. The plan continues to drift. By the time issues are obvious, they have been compounding for months.

What to do differently

Track forecast errors by department to make accuracy visible.

Close audit and control gaps early before they become distractions.

Aim for a one-day close with board materials ready by Day 2.

Assess the leadership bench early so execution risk doesn't catch you by surprise later.

In conclusion:

If you step back from these seven failure points, a pattern emerges.

By the time CAC is clearly creeping up, millions have already been spent.

By the time margin erosion is visible, discount behavior is culturally ingrained.

By the time working capital pressure shows up, liquidity is already tight.

By the time spending drifts from the thesis, the budget cycle has moved on.

By the time savings fail to hit the P&L, the organization has lost urgency.

By the time reporting exposes initiative drift, months have passed.

The Ellie Mae, Marketo, Dynatrace, and Tessara examples all share a common feature that's easy to miss. The moves worked because the organizations could connect them directly to financial outcomes quickly enough to adjust in real time.

That is what separates a 100-day plan that looks good on paper from one that actually produces value. The first 100 days are not about doing more. They are about seeing faster. Once finance can see clearly, the rest of the playbook starts to work the way it was designed.

That is the work of the first 100 days. Good luck!